Wall Street is playing a dangerous game. Here's what soaring tech is hiding about inflation, bonds, & your portfolio.

AI stocks just can’t stop rising. Sell-side Wall Street analysts are obliged to play the name-a-higher-number game and are scrambling to raise their price targets repeatedly as old ones get exceeded. Justifications are becoming more speculative. The analysts already spent all their rosiest facts justifying previous rounds of increases. Reported financial results, which are backwards looking by definition, can’t easily be stretched far enough to justify the enthusiasm. However, who is to say what the future might conceivably hold? It is always a blank slate. It needs to be different this time.

Is it possible to question the wisdom of joining the AI trade without being labeled a dinosaur or a Luddite? The multi trillion-dollar question is where all the end demand will come from? The Vanguard Information Technology ETF (VGT) has nearly tripled since early 2023. Can corporate technology budgets conceivably rise fast enough for long enough to justify that?

True, the increase approximately mirrors the capital expenditure growth of the major cloud computing companies, the ones buying all this compute. They are desperate to remain relevant in a rapidly changing landscape, whatever the cost. The question is whether end users will be willing to pay more. Technological progress has historically been a story of everything getting better and cheaper, not better and more expensive apace.

Then again, massively higher direct spending on technology might be offset by direct savings on labor. If 200 software engineers at $500,000 per head can be reduced to 50 supplemented with $20 million of yearly artificial intelligence spending, then maybe technology budgets don’t need to rise. AI providers could become more profitable while end customers do too. The losers are the 150 engineers looking for work. Technology has often been a short-term destroyer of jobs. In the long run, the labor force simply adapts. Employment data remains solid, with April’s BLS report showing unemployment steady at 4.3%, job additions beating expectations, and accompanied by a positive revision to the prior month.

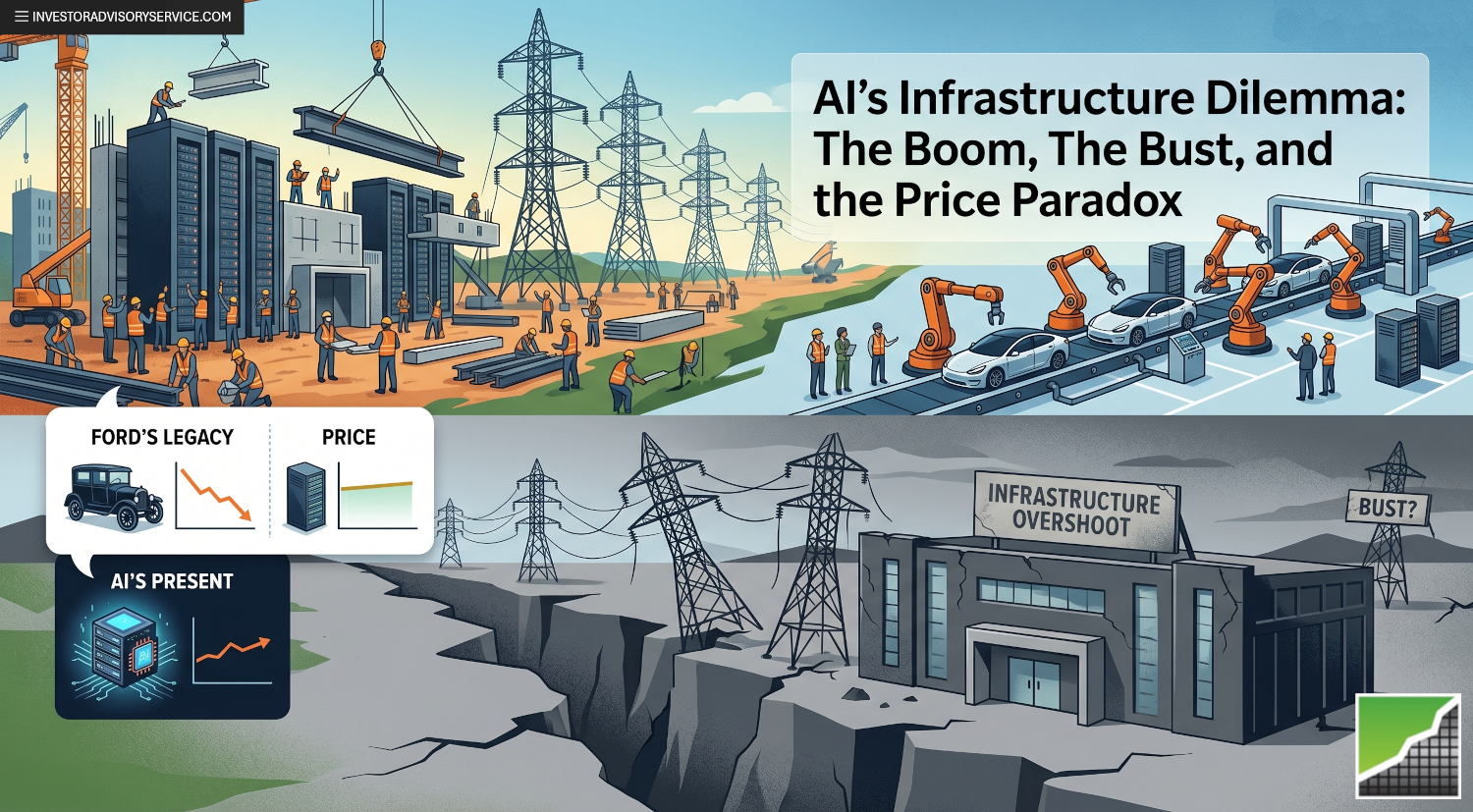

Perhaps the jobs lost to AI are being offset by gains from the massive physical build-out of datacenters, power generation, and similar infrastructure. The problem with infrastructure booms, however, is that not only can they end, but they can also overshoot and be followed by an infrastructure bust as young technologies require time to grow into their full-sized adult clothes.

It’s not for nothing. We are likely experiencing a software productivity revolution mirroring Henry Ford’s adoption of the assembly line, which was estimated to cut labor hours per finished automobile by an astounding 90%. The difference is that Ford’s productivity gains spread throughout society in the form of lower prices for vehicles. In twenty years, car ownership grew 50-fold. By contrast, it is difficult to identify goods or services that are currently becoming cheaper as a result of artificial intelligence.

Speaking of nothing getting cheaper, April’s CPI index showed 12-month consumer basket inflation of 3.8%. Energy was a major driver, rising 18%. The Iran conflict has reduced global oil supplies and closed important shipping lanes. It is reasonable to view energy inflation as acute and, dare we say, transitory. However, even without food and energy, the index still rose 2.8%. The producer price index rose 1.4% for April and is up 6.0% over the past twelve months. Again, where are the productivity gains? The answer may be corporate profits in the short term. In the long term, competition should win out. Someday AI should prove deflationary. Not yet.

Bond yields rose modestly on the “hot” inflation prints. Higher inflation generally means higher interest rates, but one never knows for sure how the bond market will react to anything. Bond investors have ever-changing expectations about inflation and, essentially, about the Federal Reserve’s response to inflation. It’s complicated. Coming into the year, markets were anticipating rate cuts. Now expectations are for the Fed to stand pat with a slight bias to a rate hike, if anything. Some recent U.S. dollar strength and gold weakness are consistent with a more hawkish Federal Reserve. New Chairman Kevin Warsh’s first Open Market Committee meeting will be in mid-June. Investors will be glued to their screens and primed to overreact when he gives his first address following that meeting on June 17.

The roaring stock market is overshadowing the bond market, as usual, but it is worth remembering that the economy runs on debt. The price of that debt matters a lot. Higher yields dampen business investment and consumer spending while also affecting people’s lives in other ways that can’t easily be measured. Mortgage lock-in describes people remaining in homes that are no longer suitable for them but that carry an attractive mortgage rate from the past. A lot of people would move if they could afford to. That frustration doesn’t show up in any data.

In recent years, the dominant narrative around yields has been that they will fall, just maybe not as fast as some people hope. On the contrary, the U.S. 10-Year Treasury yield is approaching 4.5%. Any further increase from here, and the discussion becomes whether it could next push through 5%, a level not seen since early 2007. U.K. sovereign debt just broke through that level as the market reacted to a chaotic series of local elections which saw the longstanding duopoly between Labour and Conservatives fragmented into a 5-way system. The party controlling the most local councils is suddenly the anti-tax, immigration skeptical Reform UK.

It’s not just the direction of yields that matters, but also what that direction represents. For decades, U.S. Treasury Yields almost always declined sharply during times of sudden stress. Long-term Capital Management’s implosion in 1998, September 2001, the financial crisis of 2008-09, and the Covid outbreak in February 2020 were all accompanied by sharp declines in yields. However, the surprise U.S. attack on Iran at the end of February produced the opposite effect. Yields have risen steadily since the beginning of Operation Epic Fury. This could signify that bond investors consider the situation in Iran an irrelevant sideshow and are focusing on other things. Alternatively, it could suggest that U.S. Treasuries are no longer the safe-haven asset they used to be. Intuitively, there must be a point where ballooning deficits and inconsistent economic policies jeopardize global demand for dollar-denominated obligations, turning U.S. Treasuries into simply one more “risk asset” in a world full of them. Can we really blame people if they think it’s smarter to clutch Nvidia and Apple shares?

Stock market investors have historically accepted short-term volatility and been rewarded with long-term outperformance. Certain richly valued parts of the market may threaten to reverse that equation. Stocks that seem to rise every single day are easy to own in the short term but untrustworthy in the long term. The best defense is always diversification, and we also recommend investors maintain high standards for quality. A solid company should earn you a respectable long-run return, even if you accidentally overpay for it at the outset.

Looking for high quality stock picks?

In the June 2026 issue of the Investor Advisory Service we present a mega-cap entertainment company that has become a dominant player in its space and a midsized healthcare company that looks great on the Stock Selection Guide. Subscribe today to unlock these and other top picks!

The commentary is excerpted from the issue of the Investor Advisory Service newsletter published at the end of May 2026. To receive commentary like this in a timely matter and receive actionable stock ideas each and every month, subscribe today. The Investor Advisory Service stock newsletter was named to the Hulbert Investment Newsletter Honor Roll for the 16th consecutive year for outperforming every up and down market cycle since 2007.

For more information about the Investor Advisory Service, to download a sample issue, or to subscribe to the best investing newsletter in the U.S. for long-term consistent returns, visit Investor Advisory Service.

©Equity Research Service. All Rights Reserved. Privacy Policy. Terms of Use.