Strong earnings and massive AI investment are driving the rally, but higher rates and concentrated leadership pose risks.

Since bottoming at the end of March, stocks have rebounded and are hovering near all-time highs, propelled by strong first quarter earnings. The market continues to be driven primarily by the AI theme, but companies overall had a strong first quarter, and this earnings momentum is expected to continue through the remainder of the year.

In an atypically strong showing, first quarter earnings increased more than 25%, exceeding twice consensus analyst estimates at the end of March. According to FactSet’s Earnings Insight, earnings growth in excess of 20% is expected in each quarter for the remainder of the year. Consensus full year earnings estimates have been revised higher and now reflect 23% growth versus estimates of 15% coming into 2026. Growth expectations for 2027 have also approximately doubled to 16% since January. The year-to-date move in stocks has been supported by better than anticipated fundamental performance. Multiples have drifted lower since January, with the forward P/E ratio for the S&P 500 just north of 20x, approximately in line with the five-year average.

Earnings growth continues to be supported by fiscal deficits, labor productivity gains, and a robust AI-related capital expenditure cycle. Hyperscalers are projected to spend approximately $725 billion on capital expenditures this year, increasing to more than $1 trillion in 2027, with further increases expected in 2028. Companies continue to cite strong returns on investment, supported by continued improvements in frontier models like Anthropic’s Mythos and strong overall demand.

Collectively, Amazon, Alphabet, Meta, and Microsoft generated approximately $200 billion in free cash flow in 2025. That figure is expected to drop to closer to $75 billion this year due to AI-related investments. While some have suggested hyperscaler capex might be constrained by free cash flow, the companies have tapped the capital markets. Alphabet raised nearly $85 billion in an equity offering in early June, in part to help fund spending on AI. Following Alphabet’s successful offering, according to the Financial Times, Meta was also rumored to be exploring an equity offering in the “tens of billions of dollars.” Debt issuance is also expected to help fund investment, with hyperscalers expected to issue more than $200 billion in debt this year. Given the narrow leadership of the market, a downward recalibration for the trajectory of AI spend would represent a risk to the overall market, but so far, there is little to suggest immediate concern.

The SpaceX IPO kicked off what is expected to be a parade of large private companies coming to market this year. In the largest ever IPO, SpaceX went public at a $1.8 trillion valuation, though the company raised “only” $85.7 billion. Despite valuation concerns based solely on the company’s current operations, investors continue to believe in Elon Musk’s vision to open new opportunities. Investor appetite for SpaceX was strong out of the gate, as shares gained nearly 50% over the first three days of trading.

Given expectations for the IPOs later this year of both OpenAI, which in March was valued at $852 billion in its most recent funding round, and Anthropic, which raised funds at a $965 billion valuation, there is some investor angst regarding how much the market can comfortably digest. The SpaceX IPO suggests these concerns may be overblown, and even with both OpenAI and Anthropic expected to go public later this year at a valuation of $1 trillion or more each, it is relative to the approximate $75 trillion in total U.S. stock market value.

Concerns regarding a softer labor market late last year have eased. The May jobs report was stronger than expected with 170,000 jobs added, well ahead of expectations of 80,000. The report also increased the number of jobs added in both March and April. The three months averaged payroll gains of 188,000, the strongest in more than two years. The unemployment rate remained steady at 4.3%.

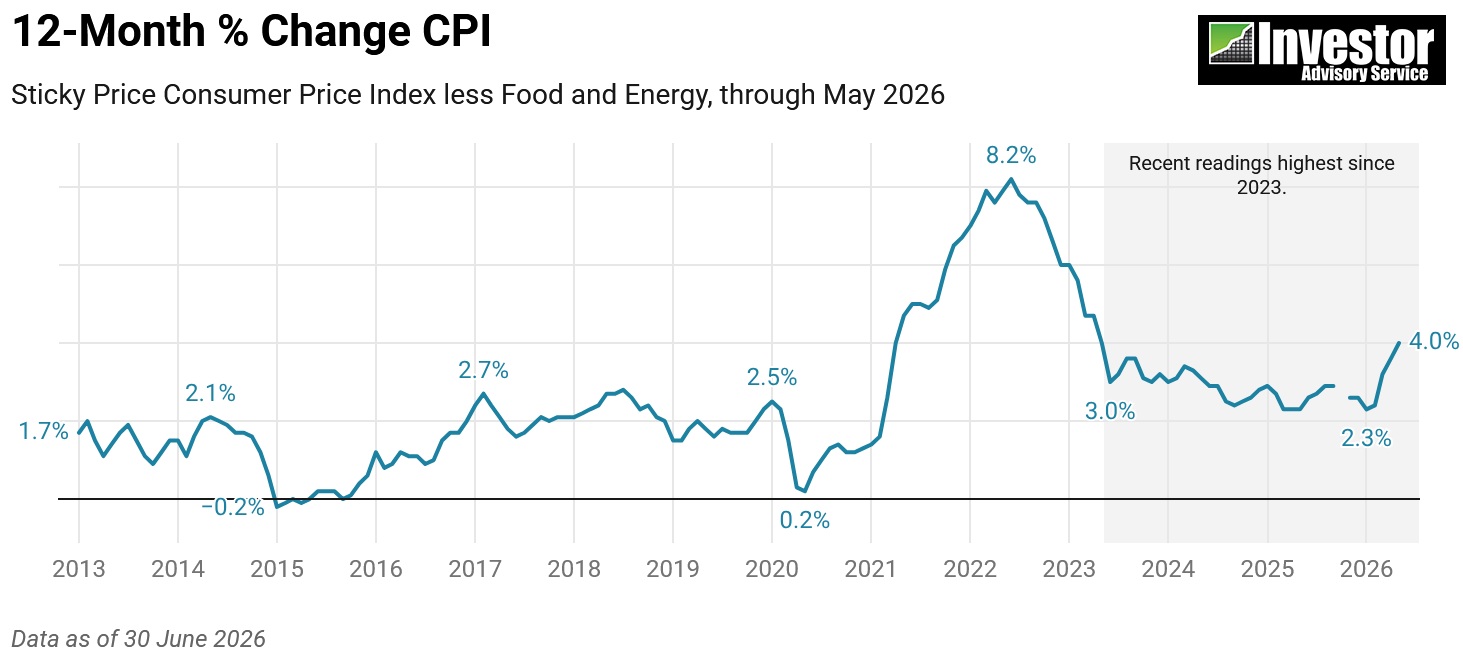

For the Federal Reserve, which carries a dual mandate of full employment and price stability, the labor report shifted the focus towards inflation, which continues to run above target and has faced upward pressure from the Iran conflict. The May Consumer Price Index (CPI) year-over-year inflation hit a three-year high of above 4.0%, due in part to higher energy costs. Excluding food and energy, core CPI rose 2.9%, in line with expectations but a tick higher than in April.

With the May PPI and CPI already released, the Fed’s preferred measure of inflation, the core Personal Consumption Expenditures Price Index (PCE), is expected to come in at 3.4%, up slightly from April and continuing to run well ahead of the Fed’s 2% target.

Coming into the year, investors were expecting two 0.25% rate cuts from the Fed in 2026, but a stronger than expected labor market coupled with inflation that continues to run above target have shifted the thinking of market participants. Following the May jobs report, expectations now reflect an expected 0.25% rate increase by the end of 2026. After the strong May jobs release, rates moved higher and stocks fell in response. The yield on 10-year Treasuries has increased from 4.2% at the start of the year to 4.4% currently, but it remains lower than the peak earlier this year of nearly 4.7%. New Fed Chair Kevin Warsh, who was nominated by a President who clearly prefers lower interest rates, will have to balance inflationary concerns and a bias toward rate increases by some voting members of the Fed. At his first press conference, Warsh emphasized the Fed’s commitment to delivering price stability.

There are signs inflation will ease, but the sources of inflationary pressure continue to shift. Supply chain effects from the pandemic, tariffs, energy shocks, the AI buildout, and wealth effects from a strong stock market have all contributed to inflation that continues to run above target. Importantly, longer-term inflation expectations remain anchored. A deal with Iran to reopen the Strait of Hormuz should help ease energy price pressures, as WTI Crude has come down from a peak of nearly $113 a barrel earlier this year to around $77 a barrel, about $10 higher than just before the conflict. Average hourly earnings in May rose 3.4% from the prior year, down from a 3.6% gain in April and matching the slowest increase since 2021. Continued gains in labor productivity would also help bring inflation down.

As always, the current environment presents reasons for both optimism and concern. Seeking growing companies that are profitable, generate attractive returns on invested capital, and are reasonably priced continues to serve as a sensible path for building a portfolio for the longer term.

Looking for high quality stock picks?

In the July 2026 issue of the Investor Advisory Service we spotlight two companies that have been covered previously but present reasonable opportunities at their current valuations. Subscribe today to unlock these and other top picks!

The commentary is excerpted from the issue of the Investor Advisory Service newsletter published at the end of June 2026. To receive commentary like this in a timely matter and receive actionable stock ideas each and every month, subscribe today. The Investor Advisory Service stock newsletter was named to the Hulbert Investment Newsletter Honor Roll for the 16th consecutive year for outperforming every up and down market cycle since 2007.

For more information about the Investor Advisory Service, to download a sample issue, or to subscribe to the best investing newsletter in the U.S. for long-term consistent returns, visit Investor Advisory Service.

©Equity Research Service. All Rights Reserved. Privacy Policy. Terms of Use.